Optimize Your Benefits with VA Home Loans: Lower Interest Fees and Flexible Terms

Optimize Your Benefits with VA Home Loans: Lower Interest Fees and Flexible Terms

Blog Article

Browsing the Home Loans Landscape: Exactly How to Utilize Funding Solutions for Long-Term Wealth Structure and Security

Navigating the intricacies of home loans is important for anyone looking to build wealth and make certain economic protection. Recognizing the various kinds of funding alternatives readily available, along with a clear assessment of one's monetary circumstance, lays the foundation for notified decision-making.

Comprehending Home Mortgage Types

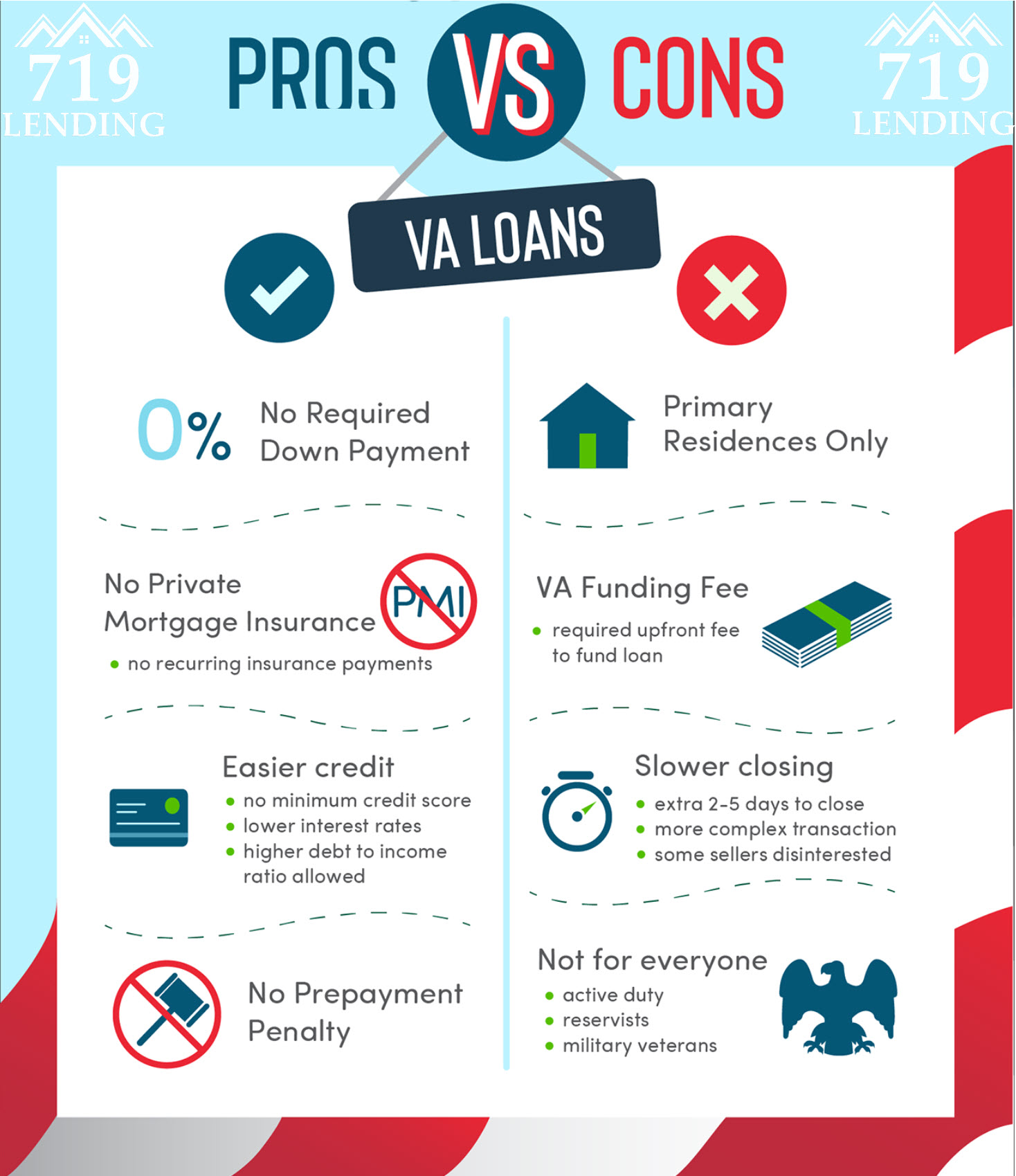

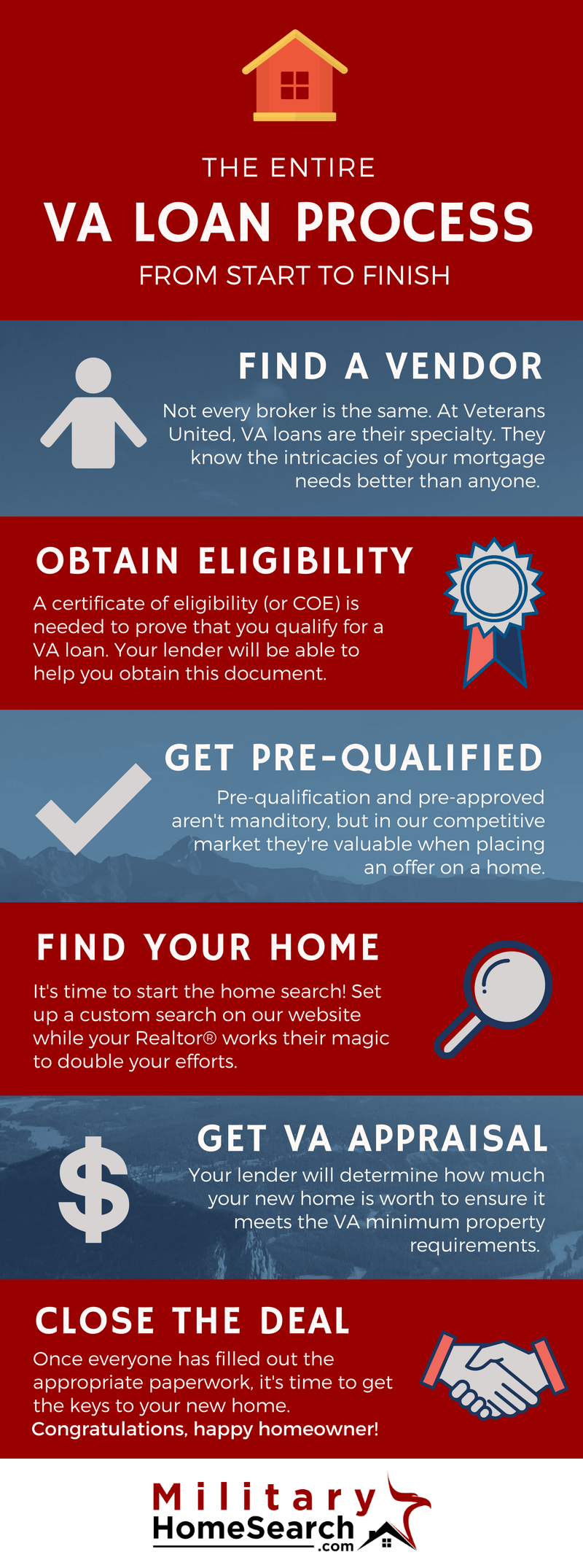

Mortgage, a critical component of the realty market, come in various types developed to meet the diverse needs of customers. The most common kinds of home mortgage include fixed-rate mortgages, variable-rate mortgages (ARMs), and government-backed fundings such as FHA and VA financings.

Fixed-rate home mortgages provide stability with consistent month-to-month repayments throughout the lending term, normally varying from 15 to 30 years. In contrast, ARMs include rate of interest rates that fluctuate based on market problems, frequently resulting in reduced initial settlements.

Government-backed fundings, such as those guaranteed by the Federal Housing Management (FHA) or guaranteed by the Department of Veterans Matters (VA), deal with details groups and commonly require lower deposits. These fundings can assist in homeownership for individuals who might not qualify for traditional funding.

Evaluating Your Financial Circumstance

Assessing your financial situation is an essential action in the home mortgage process, as it lays the foundation for making educated loaning decisions. Begin by assessing your revenue sources, consisting of salaries, perks, and any kind of additional revenue streams such as rental homes or investments. This extensive view of your revenues aids lenders establish your borrowing capacity.

Following, examine your expenses and month-to-month responsibilities, including existing financial debts such as credit scores cards, student loans, and auto repayments. A clear understanding of your debt-to-income ratio is crucial, as a lot of lenders favor a ratio listed below 43%, ensuring you can take care of the new home mortgage payments along with your present obligations.

Additionally, assess your credit history, which significantly influences your finance terms and rate of interest. A greater credit history shows monetary reliability, while a reduced score might require approaches for improvement prior to obtaining a lending.

Lastly, consider your possessions and savings, consisting of reserve and fluid financial investments, to ensure you can cover deposits and shutting expenses. By meticulously examining these parts, you will be better placed to browse the home mortgage landscape effectively and protect funding that aligns with your long-term financial goals.

Techniques for Smart Borrowing

Smart borrowing is necessary for browsing the intricacies of the home loan market efficiently. To enhance your borrowing technique, begin by comprehending your credit rating profile. A strong credit rating can significantly lower your rate of interest, equating to substantial savings over the life of the finance. Frequently checking your credit record and resolving disparities can enhance your rating.

Following, take into consideration the type of home loan that ideal matches your financial situation. Fixed-rate loans use security, while variable-rate mortgages may provide lower first payments but carry risks of future rate boosts (VA Home Loans). Evaluating your long-term why not try this out plans and monetary ability is vital in making this decision

Additionally, objective to secure pre-approval from loan providers before home hunting. When making an offer., this not just offers a clearer image of your budget plan but additionally enhances your negotiating position.

Long-Term Riches Building Methods

Building long-term wide range with homeownership calls for a calculated strategy that goes beyond merely safeguarding a mortgage. One effective method is to think about the admiration possibility of the home. Choosing homes in expanding areas or locations with intended developments can lead to considerable boosts in residential property worth with time.

One more important element is leveraging equity. As home mortgage payments are made, house owners develop equity, which can be touched into for future investments. Utilizing home This Site equity financings or lines of debt carefully can offer funds for additional property financial investments or renovations that better boost building worth.

Moreover, preserving the residential or commercial property's condition and making strategic upgrades can dramatically add to long-lasting riches. Straightforward renovations like modernized bathrooms or energy-efficient devices can generate high returns when it comes time to sell.

Finally, understanding tax obligation benefits associated with homeownership, such as mortgage interest deductions, can improve monetary outcomes. By making best use of these advantages and adopting a proactive financial investment attitude, property owners can cultivate a durable profile that fosters long-term wide range and security. Ultimately, a well-rounded approach that prioritizes both home selection and equity monitoring is necessary for sustainable wide range structure with realty.

Maintaining Financial Safety And Security

In addition, fixed-rate home mortgages use predictable monthly payments, enabling better budgeting and financial planning. This predictability safeguards homeowners from the fluctuations of rental markets, which can lead to sudden increases in housing costs. It is essential, nonetheless, to make certain that home mortgage repayments remain convenient within the more comprehensive context of one's monetary landscape.

Furthermore, responsible homeownership entails normal upkeep and renovations, which secure building value and enhance total safety and security. Homeowners need to also take into consideration diversifying their economic portfolios, making certain that their investments are not only tied to property. By incorporating homeownership with other economic instruments, people can produce a well balanced method that minimizes risks and improves overall monetary stability. Inevitably, maintaining financial security with homeownership calls for a informed and positive approach that emphasizes cautious preparation and recurring diligence.

Final Thought

In final thought, successfully browsing the home lendings landscape necessitates an extensive understanding of various car loan types and an extensive analysis of specific financial situations. Implementing critical loaning practices helps with lasting wealth buildup and safeguards financial security.

Browsing the intricacies of home finances is essential image source for anyone looking to build wide range and guarantee economic safety and security.Evaluating your monetary scenario is a vital step in the home finance process, as it lays the structure for making educated borrowing choices.Homeownership not just serves as an automobile for lasting wealth structure yet also plays a substantial role in preserving economic security. By integrating homeownership with various other financial tools, people can produce a well balanced approach that reduces threats and enhances overall economic stability.In verdict, successfully browsing the home finances landscape demands a comprehensive understanding of different financing types and a detailed assessment of private monetary circumstances.

Report this page